Stay up To Date

March 2026 Bend Housing Market Update

Stay up To Date

February’s numbers continue the story that began in January. What initially looked like a modest seasonal pickup is starting to show clearer signs of momentum building in the market. More sellers are entering the market as we move toward spring, but buyers are stepping forward at the same time. When both sides of the market begin to move together, the result is often a market that feels busier without dramatically shifting negotiating leverage in either direction. For both buyers and sellers, the biggest risk right now is assuming the market is either “slow” or “hot.” In reality, it is increasingly selective.

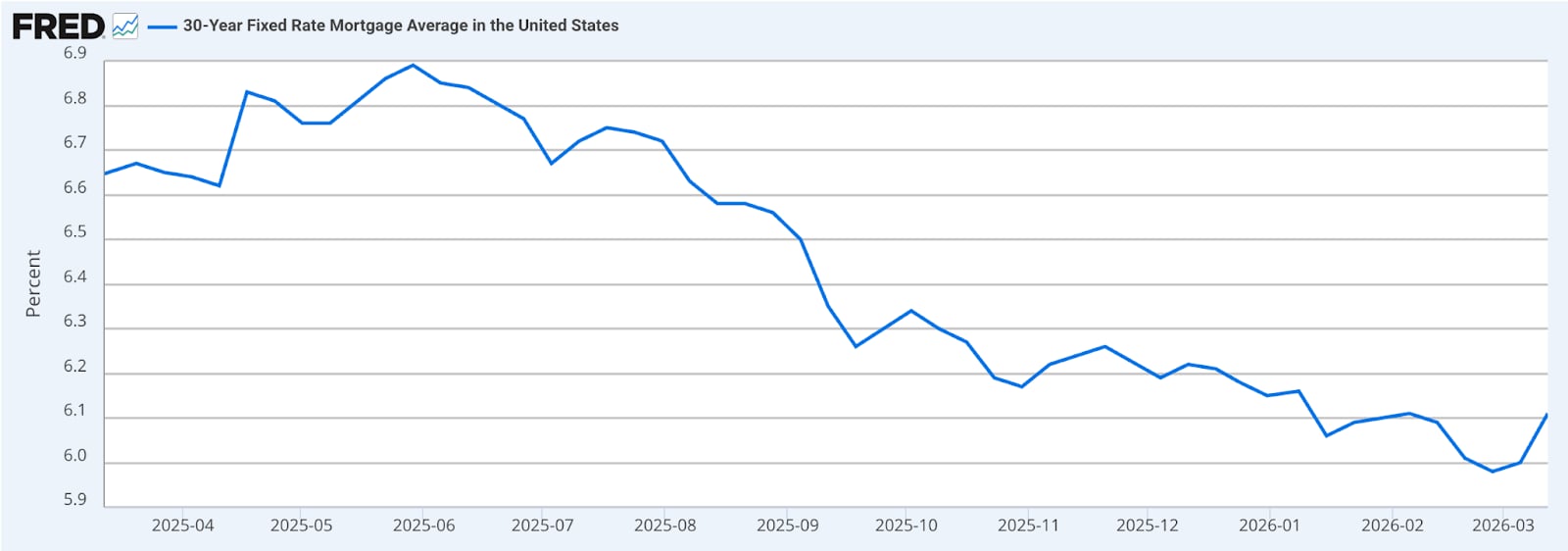

Overall, mortgage rates have been relatively stable and near 6% for a number of weeks. This is a level that really was only seen once in 2024 and once in 2023. Compared to where rates were sitting this time last year, this still represents a meaningful improvement in affordability. We are beginning to see the impact of that in the composition of buyers. Cash purchases made up 28.7% of February sales, which is noticeably lower than the 36.4% share we saw at this time last year. That shift suggests financed buyers are becoming more active again. For much of 2024 and early 2025, higher borrowing costs pushed many financed buyers to the sidelines and allowed cash buyers to represent a larger share of the market. As rates have improved, that balance appears to be normalizing. A broader buyer pool generally creates a healthier and more stable housing market.

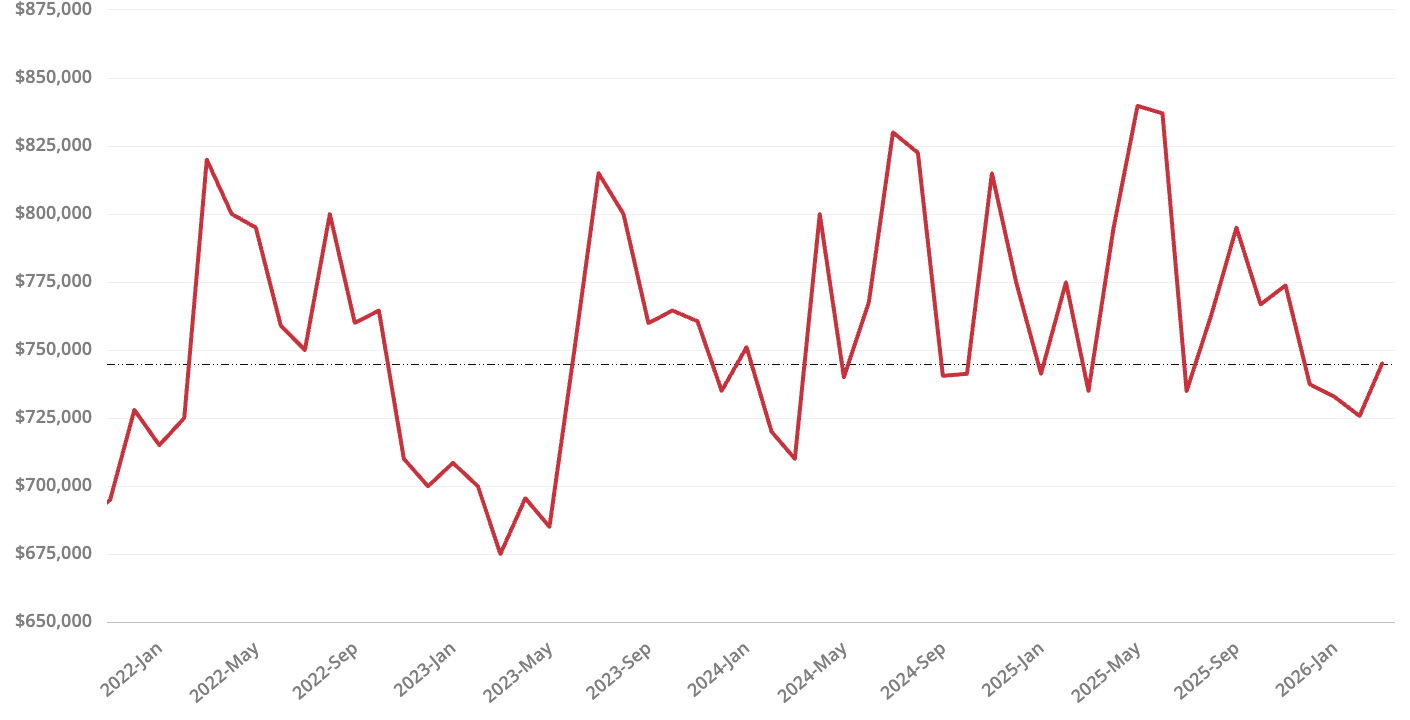

The median home price in February rose to $745,000, up from $735,000 in January. On a month-to-month basis, that represents a modest increase of about 1.4%. While one month of data does not establish a trend, it reinforces a pattern we have been watching for several months. Prices are not experiencing rapid appreciation, but they are also not showing signs of widespread decline. Instead, the market appears to be stabilizing within a relatively narrow range. For buyers, this stability creates an environment where affordability is not being eroded by rapid price increases. For sellers, it reinforces the importance of pricing correctly. In a market where prices are moving gradually rather than quickly, overpricing rarely produces the desired result.

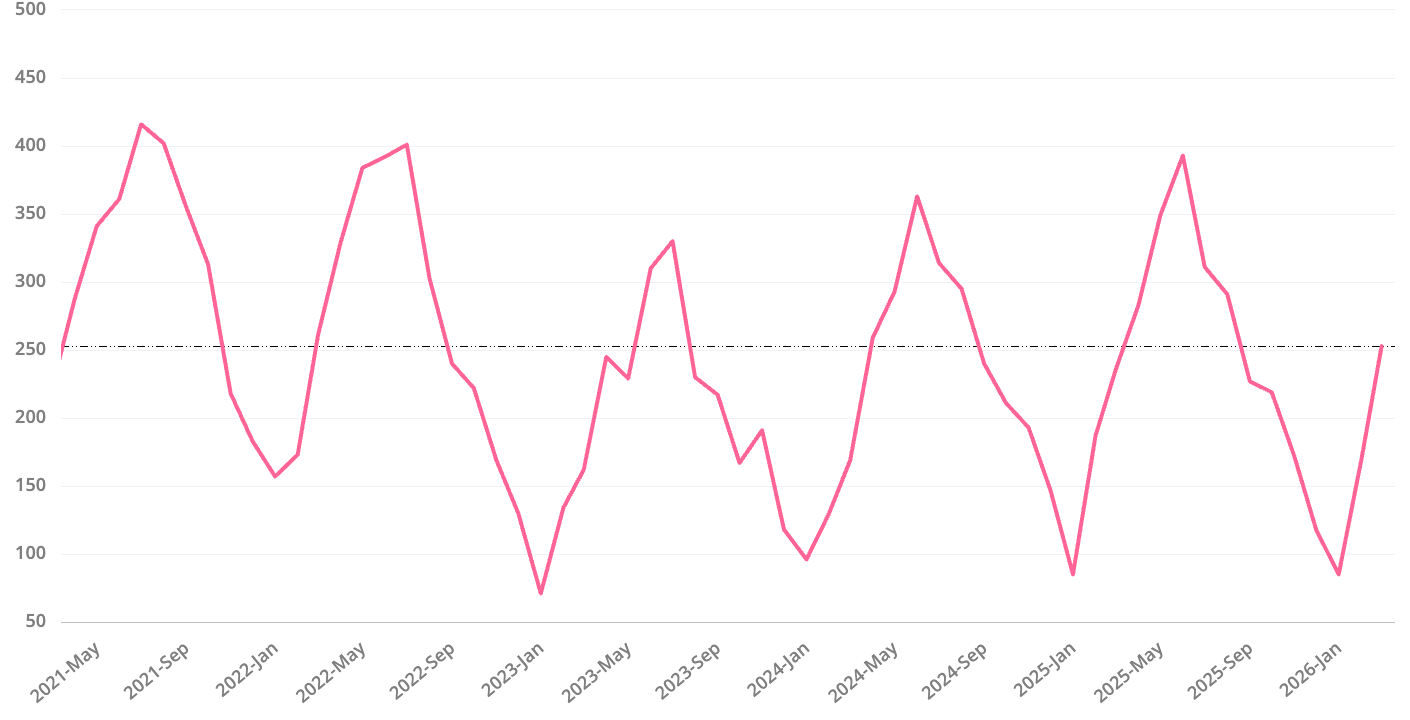

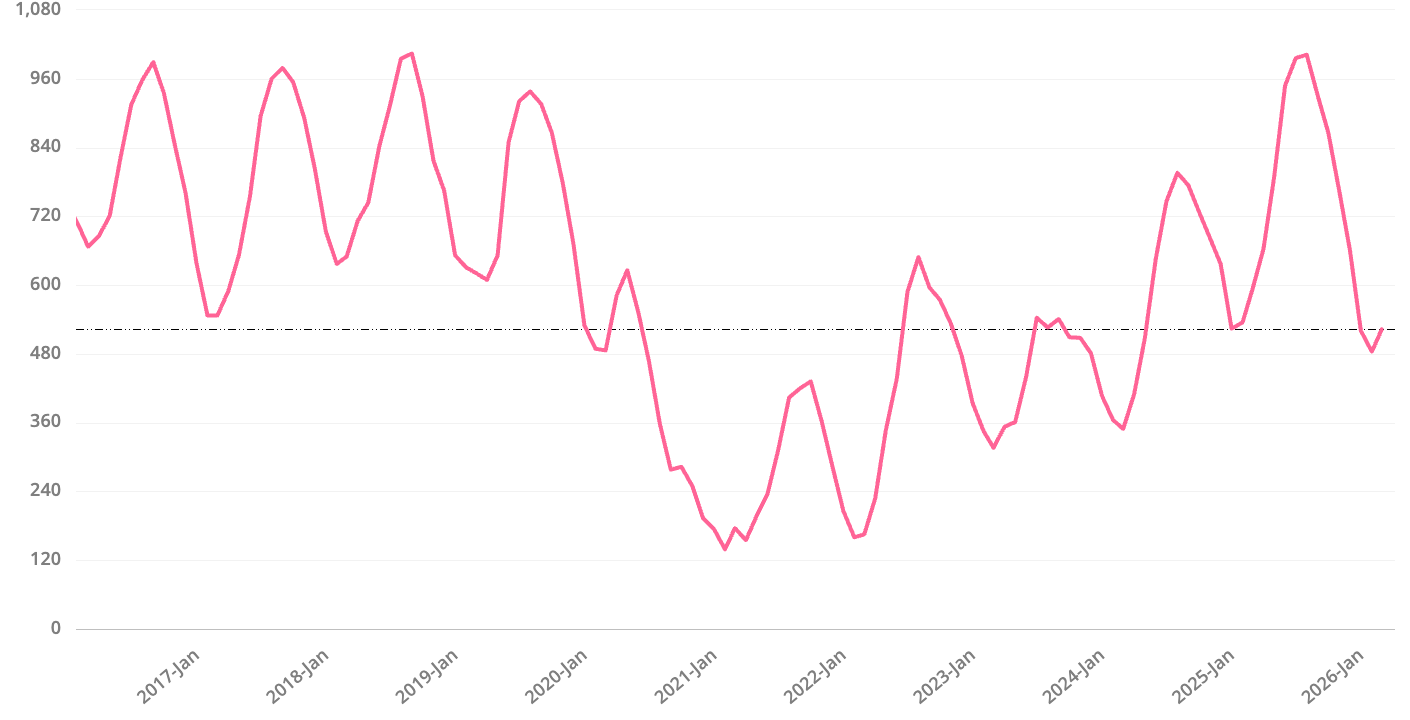

February brought 253 new listings to the market. That is a significant increase from January’s 166 new listings, which is consistent with the seasonal pattern we typically see as we approach the spring selling season. What is more notable is that February’s new listing count is also slightly higher than the 236 new listings recorded in February of last year. This suggests that more homeowners may be willing to test the market this spring compared to early 2025. One possible explanation is the gradual improvement in mortgage rates. The “rate lock” effect that discouraged many homeowners from selling over the past two years may be beginning to soften. While many homeowners still hold very low mortgage rates, today’s borrowing costs are less restrictive than they were a year ago. Another reason could be that we saw more homes come off the market at the end of 2025 than we have since 2017. Perhaps this is the start of some of those homes coming back on the market?

Pending sales increased to 167 in February, up from 154 in January. This is one of the most important indicators in the report because pending sales reflect current buyer activity, rather than contracts written weeks or months earlier. Closed sales also increased, rising to 143 homes, up from 119 in January. However, closed sales lag the market because they reflect deals negotiated in prior weeks, so pending sales often provide a clearer real-time picture of demand.

Inventory increased from 464 active homes in January to 523 homes in February. While that is a healthy increase month to month, it is still below the 593 homes available at this time last year. This combination is important. When inventory rises but demand rises with it, the additional supply does not necessarily translate into more negotiating power for buyers. Instead, it often results in a market that becomes more active without becoming dramatically easier or harder for either side.

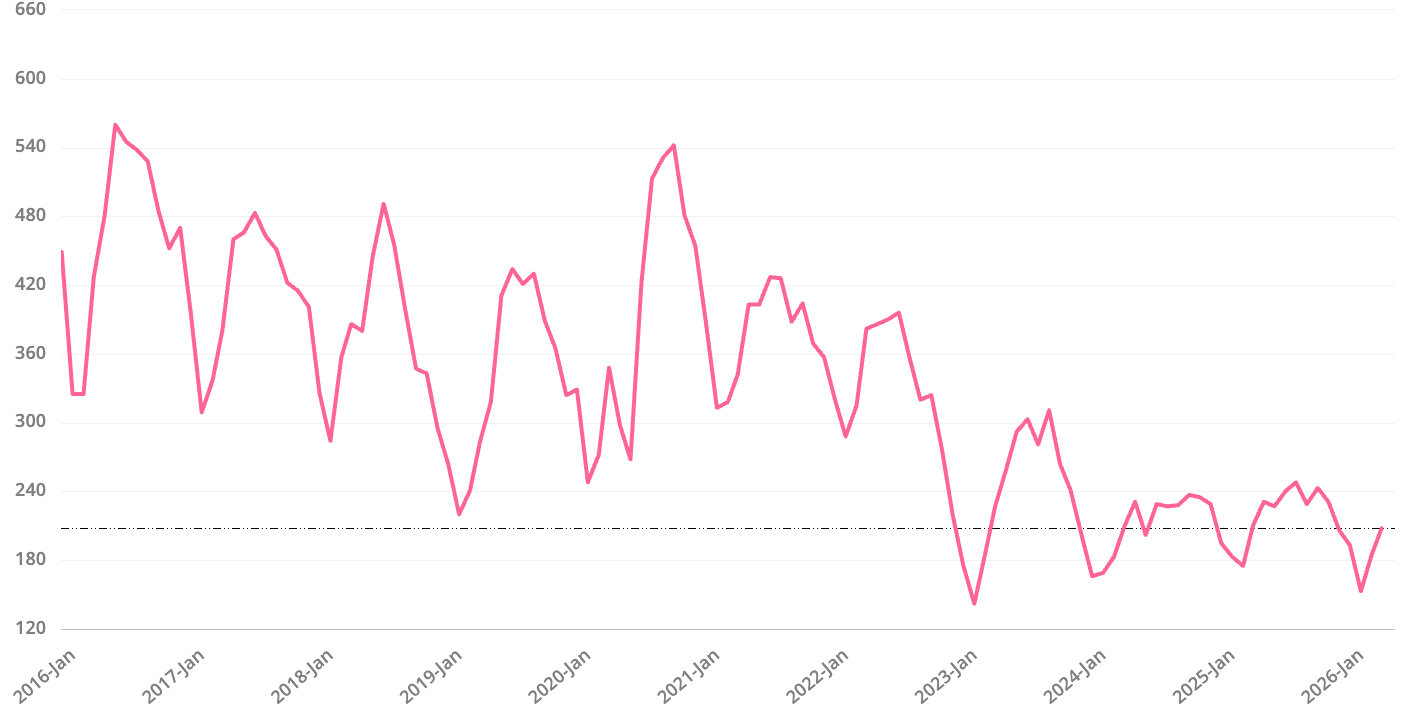

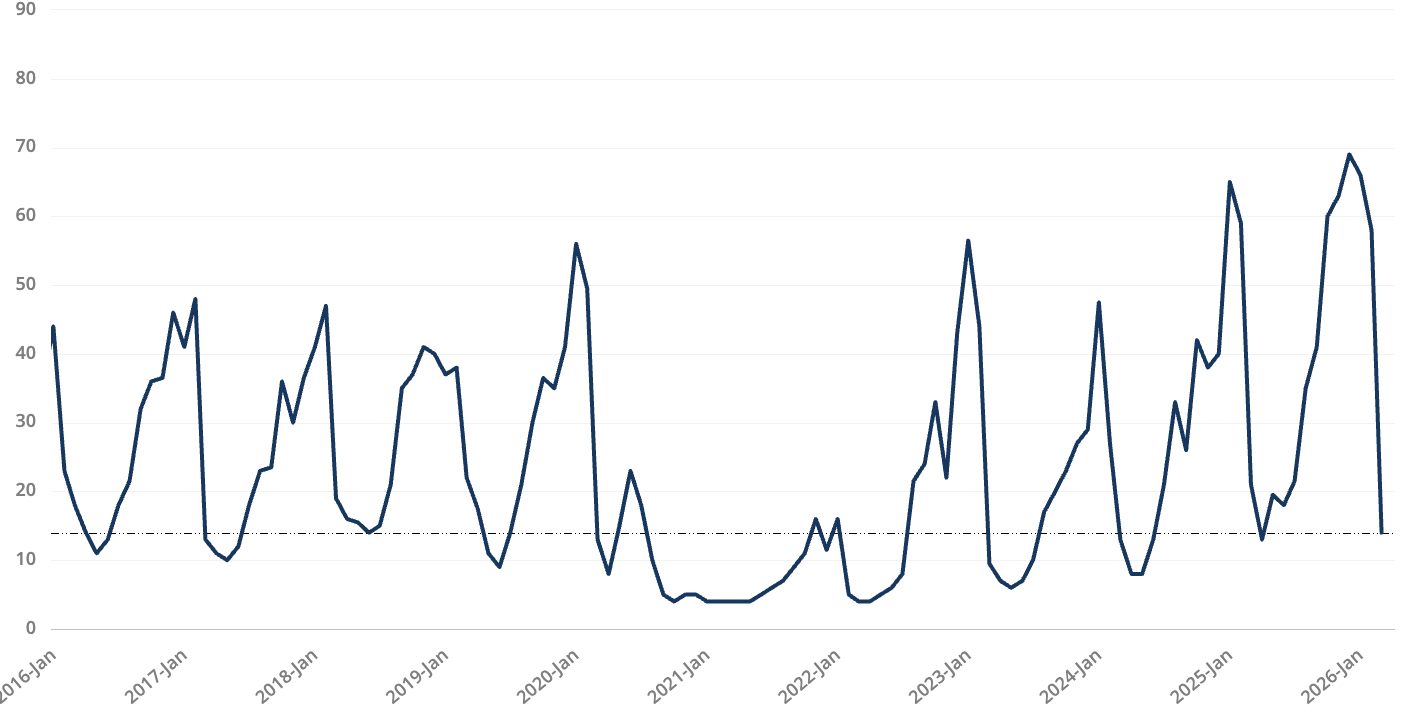

Homes that went pending in February averaged 14 days on market, a sharp drop from the 58 days we saw in January. Part of this change is seasonal, but it also suggests that well priced homes are beginning to move quickly again as buyer activity increases. This is a pattern we often see at the start of the spring market. For buyers, this may signal that the window of maximum negotiating leverage could begin narrowing as the market becomes more competitive. For sellers, it reinforces that homes positioned correctly are still capable of generating strong interest relatively quickly.

Negotiation: Homes sold in February at 98.2% of final list price, compared to 97.7% in January. Buyers are still negotiating, but the gap between asking price and final sale price has narrowed slightly.

Price Changes: At the same time, the average sale-to-original-list price ratio was 94.1%, meaning that on average, sellers reduce price by about 4.1% before negotiating further. Please note that this is up a little over 1% in the last month, meaning that things are tightening a bit as we head into spring.

Closed with Concessions: Last month 40.6% of sales closed with the seller offering some type of credit or concession. This could be a credit for closing costs, to make repairs, buy down an interest rate, etc. For perspective, this is more than double what it was in 2022, up slightly from this time last year, but down from about 50% in late 2025. Prices may be holding firm, but sellers are still needing to incentivize buyers in other ways.

February’s numbers suggest the Bend housing market is gradually gaining momentum as we move toward the spring season. Both listings and buyer activity are increasing, creating a more active environment without dramatically shifting the balance of power in either direction. For buyers, opportunities still exist, but the most desirable homes may begin moving more quickly as competition increases. For sellers, improving buyer activity is encouraging, but competition from other listings will also grow as more homes enter the market.

The early months of 2026 are showing a market that is becoming more active while remaining disciplined, and the coming months will reveal whether that balance between supply and demand continues as the spring market unfolds.

We hope you find this information valuable and that it helps you move toward your real estate goals. If you have any questions about this month’s data or would like to explore how it applies to your specific situation, please reach out to your Ladd Group broker. If you do not have one, you can reach me directly at [email protected] or on my cell at 541-280-2132.

There are also several ways to reach the team, so please let us know how we can help.

How Bend Homeowners Can Make the Right Choice for Their Home and Resale Value.

A Closer Look at the Lifestyle, Landscape, and Culture Drawing People to Central Oregon.

A Lifestyle-Driven Look at Central Oregon Living, Outdoor Access, and Community Appeal.

What Buyers Look For and How Homeowners Can Protect Long-Term Value.

Our goal is to be informative and helpful. Through our service we hope to earn your business with our exemplary level of service and extensive local knowledge of the Bend, Oregon area.

THE LADD GROUP

[email protected]

541.633.4569

CASCADE HASSON SOTHEBY'S INTERNATIONAL REALTY

650 SW Bond St

Bend OR 97702